In the past, banks effectively ‘owned’ their customers’ data, and controlled the way that this data could be accessed.

Opening access to banking data

Under new regulations, notably the Open Banking Standard in the UK and the Second Payment Services Directive (PSD2) in the European Union, this is no longer the case. Since January 2018, banking data has been accessible directly by customers or regulated third parties acting with their consent. This means that corporations and individuals are now able to access their data and initiate transactions in the manner and timing of their choice.

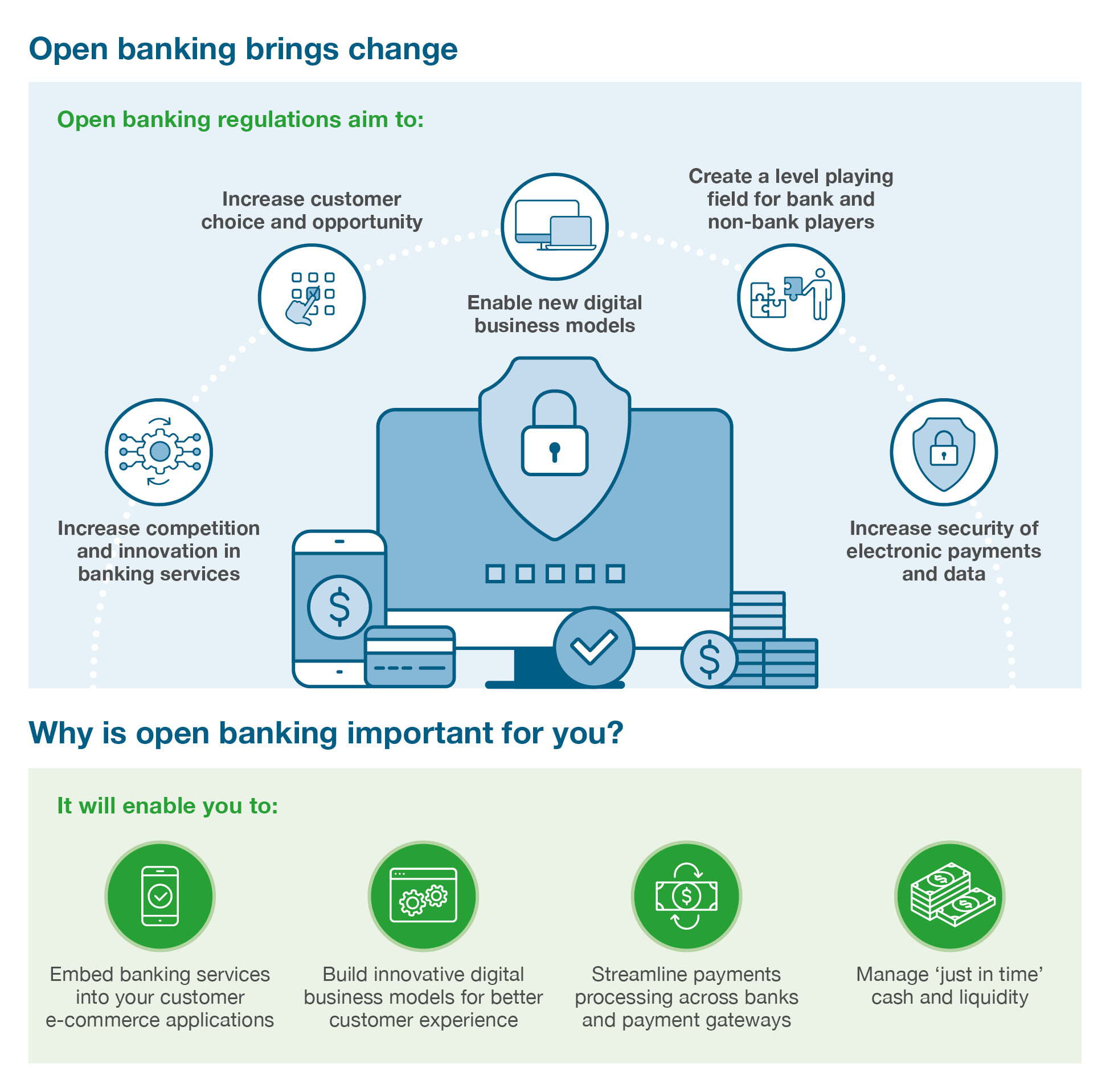

The move towards open banking marks a major change in the payments industry. By introducing the new rules, regulators aim to increase competition and innovation in banking services and ensure that both banks and fintechs offering payment services are subject to the same regulations.

For corporations, these regulations will ultimately give greater choice and flexibility in how they source data, connect and transact with banking partners and third-party payment gateways. The use of application programming interfaces (APIs) underpins open banking. These enable developers to embed third party data and services, such as banking services, directly into their applications.

Global momentum towards open banking

PSD2 applies in all EU member states, and the Open Banking Standard in the UK. In addition, open banking regulations have been introduced in jurisdictions such as Australia, Hong Kong, India and Singapore. In the UK, there were 267 regulated open banking providers in July 2020, comprising 77 banks and 190 third parties, of which 87 had at least one live solution in operation1. Digital banks such as Monzo (UK), Starling (UK), N26 (Germany) and Fidor (Germany) have emerged strongly, as well as digital lenders such as Klarna (Sweden).

As well as aiming to increase convenience and choice for consumers and businesses, open banking regulations are a response to changing business models, and in particular the rise of e-commerce. Increasingly, business is conducted in real-time, with the expectation of immediate fulfilment. Instant payment is integral to the success of e-commerce business models, which has led to the rise of new payment methods such as PayPal, ApplePay, Alipay and WeChat, as well as instant national payment schemes.

These support a real-time experience, but with the rise of new players, and new ways of conducting business, these regulations provide greater security for electronic payments and protection of financial data.

1 https://www.openbanking.org.uk/about-us/latest-news/open-banking-highlights-july-2020/

Instant payment is integral to the success of e-commerce business models, which has led to the rise of new payment methods such as PayPal, ApplePay, Alipay and WeChat, as well as instant national payment schemes.

Leveraging open banking in your business

For companies with significant e-commerce activities, particularly across borders or in multiple jurisdictions, the use of APIs, often in conjunction with other bank services, can simplify the exchange of data and transactions. This enables greater interoperability through the use of standards, implementation of rigorous authentication mechanisms and bespoke capabilities.

Most open banking initiatives to date have been targeted at consumers; however, the next 12-24 months could see significant developments in areas such as multi-bank connectivity and cross-border commerce, whether for accessing data or initiating transactions. Open banking creates the opportunity for treasurers and finance managers to develop their strategic, as opposed to transactional role within their organisations.

Many large multinational corporations have a mature bank connectivity strategy, such as using SWIFT to connect with their banking partners. However, treasurers are increasingly looking for ways to exchange data more frequently and consistently with their banks and third-party payment gateways, including in real-time. By doing so, they can consolidate data from multiple banks to provide a 360-degree view of their cash position to manage ‘just in time’ liquidity, risk and working capital more effectively. In addition, treasurers should also be looking at where points of friction or omission exist, such as lags in information flows and ‘nuisance’ accounts that are not included in existing connectivity strategies and discussing with their banks and third-party providers how APIs might resolve these issues.

For companies with significant e-commerce activities, particularly across borders or in multiple jurisdictions, the use of APIs, often in conjunction with other bank services, can simplify the exchange of data and transactions. This enables greater interoperability through the use of standards, implementation of rigorous authentication mechanisms and bespoke capabilities. For example, companies operating internationally, and selling in local currency, have to deal with the resulting currency exposure. By using APIs for connectivity, companies can access instant FX rates on transactions and convert the funds to an operating currency, avoiding FX risk and minimising the administrative effort of managing or transferring foreign currency balances.

Promoting collaboration for innovation

Open banking will create radical change, and prompt innovative ways to use artificial intelligence (AI), machine learning and robotic process automation to streamline, automation and build greater insight into payments and data processing and analytics.

On one hand, open banking creates new opportunities for third parties, such as fintechs, to ‘own’ customer relationships, potentially increasing already strong competition and disintermediating existing bank relationships and services. However, fintechs will also be subject to more regulation than in the past, offering better protection for customers, but also creating a more level playing field with banks. Therefore, just as regulated fintechs are eligible to deliver more digital banking services, so too can banks.

Many corporate clients have expressed security concerns about working with a wider range of less familiar vendors, and prefer to deal with a trusted bank to lead on new solutions. Consequently, at Standard Chartered, we are partnering with pioneering fintechs to develop new value propositions that directly meet the evolving needs of our customers.

Ultimately, while many open banking initiatives have focused first on retail and commercial banking clients, corporate and institutional clients are ultimately seeking the same level of ease, convenience and speed, which will drive further solutions and new business propositions.

Open banking expertise across our network

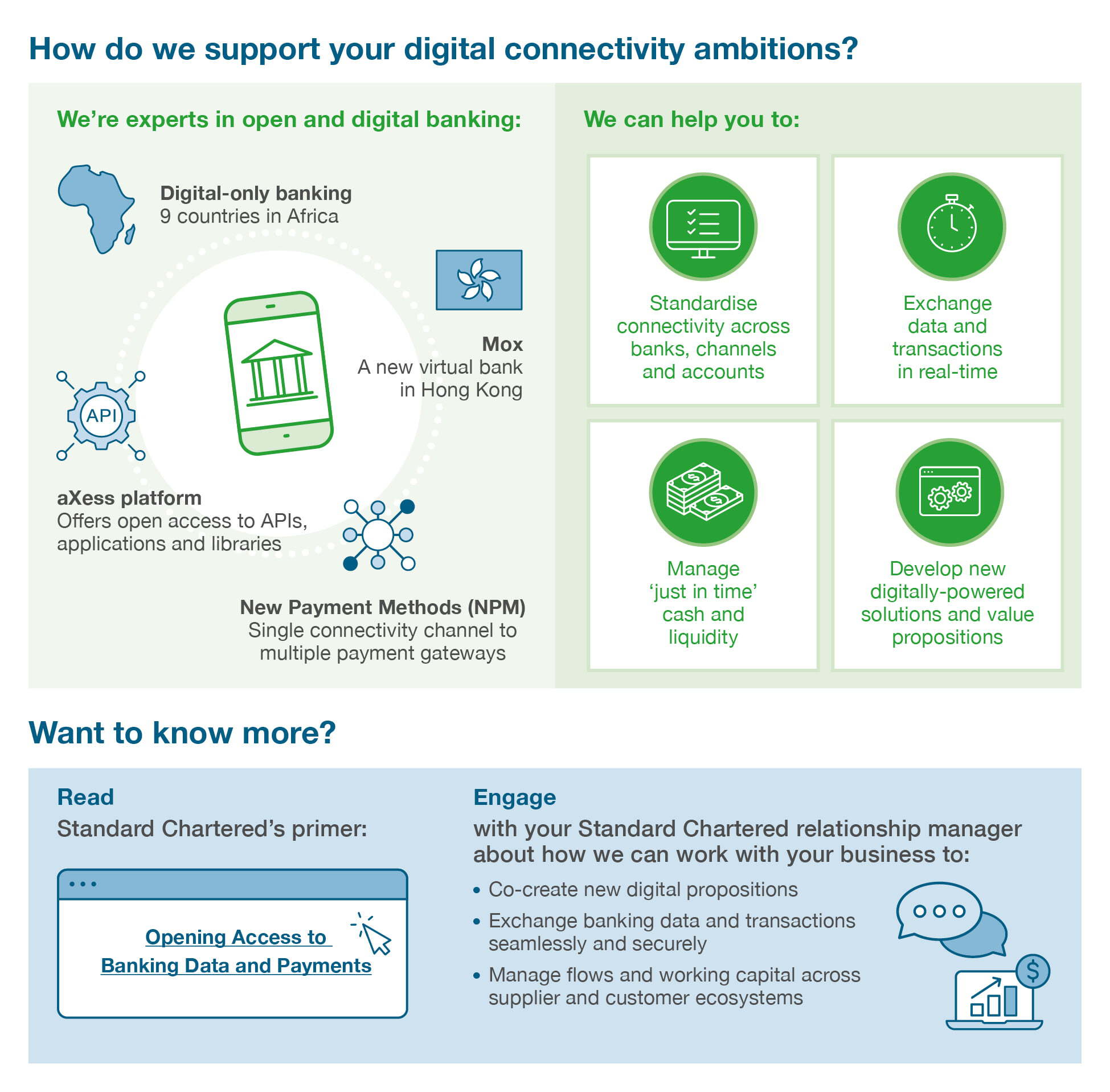

We are excited about the opportunities that open banking creates both for our clients and the bank and we are working with clients to leverage these opportunities, such as intraday reporting and balance transfers. We have introduced digital-only banking services in nine African countries in 2018 – 2019, and ramped up digital banking services in other jurisdictions. In Hong Kong, we launched Mox, a new virtual bank, with plans too to launch a similar enterprise in Singapore. Through our aXess platform, we offer open access to our APIs, applications and libraries to our clients, partners and fintechs to promote and co-create innovative banking services that support our clients’ digital connectivity ambitions.

Many of our existing solutions already follow the direction of open banking, reflected in our partnership with SAP Ariba, which allows clients to connect with multiple banks directly from the SAP Ariba platform. Our APIs are now widely used, particularly in Asia Pacific. Although initial interest was from digital and e-commerce clients, we are now seeing considerable take-up from a wide range of industries, such as insurance, auto, FMCG, amongst others, for instant policies and distributor incentive programmes. Our New Payment Method (NPM) solution offers a single channel to connect with multiple third-party payment gateways, such as Worldpay from FIS, PayPal and Stripe. Over the next 12-24 months, we expect to see compelling new solutions emerge to take advantage of open banking, and we look forward to remaining central to these initiatives that offer demonstrable value to our clients.

Although initial interest was from digital and e-commerce clients, we are now seeing considerable take-up from a wide range of industries, such as insurance, auto, FMCG, amongst others, for instant policies and distributor incentive programmes.

Embedding payments into your digital strategies